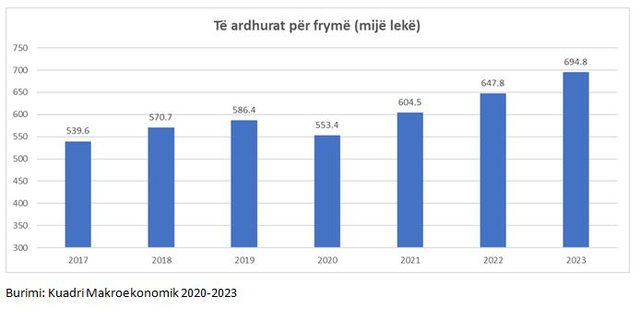

In the latest macroeconomic framework, the Albanian government predicts that per capita income in 2020 will drop to 553 thousand ALL (about 4,760 euros). Compared to a year ago, these incomes are expected to fall by 5.7%, or about 270 euros less for each Albanian.

This is the first time, at least in the last decade, that per capita income is estimated to be declining. The main reason is related to the consequences that the Covid pandemic has had on the economy. For the country's 2.84 million inhabitants, the total revenue loss is estimated at around 770 million euros.

The loss of these revenues, according to the government's forecast, is expected to recover rapidly in the coming years, reaching 604 thousand ALL (GDP per capita) in 2021 and 648 thousand ALL in 2022.

According to the forecasts in the Macroeconomic Framework, after the strong review in 2020, currently projected at -4.3%, the economy is expected to recover in 2021 and continue the positive trend in the medium term. Economic growth is projected at 5.9% in 2021 and will continue to stay close to the level of 4% during the following medium term. More specifically, economic growth is projected at 3.8 and 3.9% respectively for 2022 and 2023.

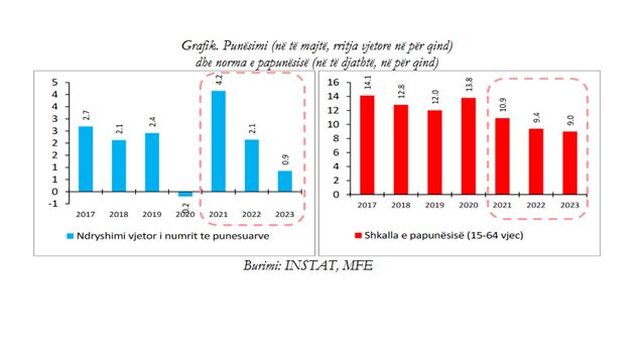

The macroeconomic framework predicts that the unemployment rate will increase to 13.8% in 2020, from 12% at the end of 2019, while the number of jobs will decrease slightly by 0.2%. But the recovery is expected to be strong and unemployment is expected to fall again to 10.9% in 2021 and 9.4% in 2022.

In line with medium-term growth forecasts, employment is expected to grow at an average of about 2.4% per year during 2021–2023. The higher labor force participation rate will be the main generator of labor supply growth. While the increase in labor demand is expected to reflect more or less the same structure of the aggregate supply perspective of economic activity.

Consequently, services are expected to contribute more to the increase in labor demand compared to other sectors of the economy. Despite the expected expansion of employment in the medium term, overall labor productivity is still expected to improve slightly during this period.

Where will the growth come from

In the medium term, growth is expected to be generated mainly by domestic demand, both private consumption and investment. Meanwhile, net foreign demand (export-import) is expected to have an almost neutral effect. Private consumption is expected to be driven mainly by improved consumer confidence as well as improvements in the labor market. The latter are expected to be transmitted in a gradual increase of wages which will further stimulate the real disposable income of individuals, creating the effect of the second round in stimulating consumption, as well as intensifying the tendency of consumers for further financing. consumer through a higher lending.

Meanwhile, consumer borrowing is projected to be driven by improved financial conditions of households, as well as the expected easing of lending standards by the banking system in the medium term, after overcoming the negative effect of the pandemic.

While the gradual increase of investments is expected to be driven by a more intensified use of existing production capacities, as well as by the acceleration of economic activity during the forecast period and the improved business perception on the medium and long term economic outlook. At the same time, improving financial conditions and easing lending standards are expected to be an important incentive for private investment in the medium term.

Specifically, total final consumption for the medium term (2021–2023) is projected to increase in real terms by an average of about 3.8% per year, contributing an average of about 3.4 percentage points per year to GDP growth. While total investments in the economy are projected to increase in real terms above 3.1% in 2021–2023, with an average contribution to total growth of about 0.7 percentage points per year.

Source: Monitor